Atom Go Tian

Senior Data Analyst

Ray White Group

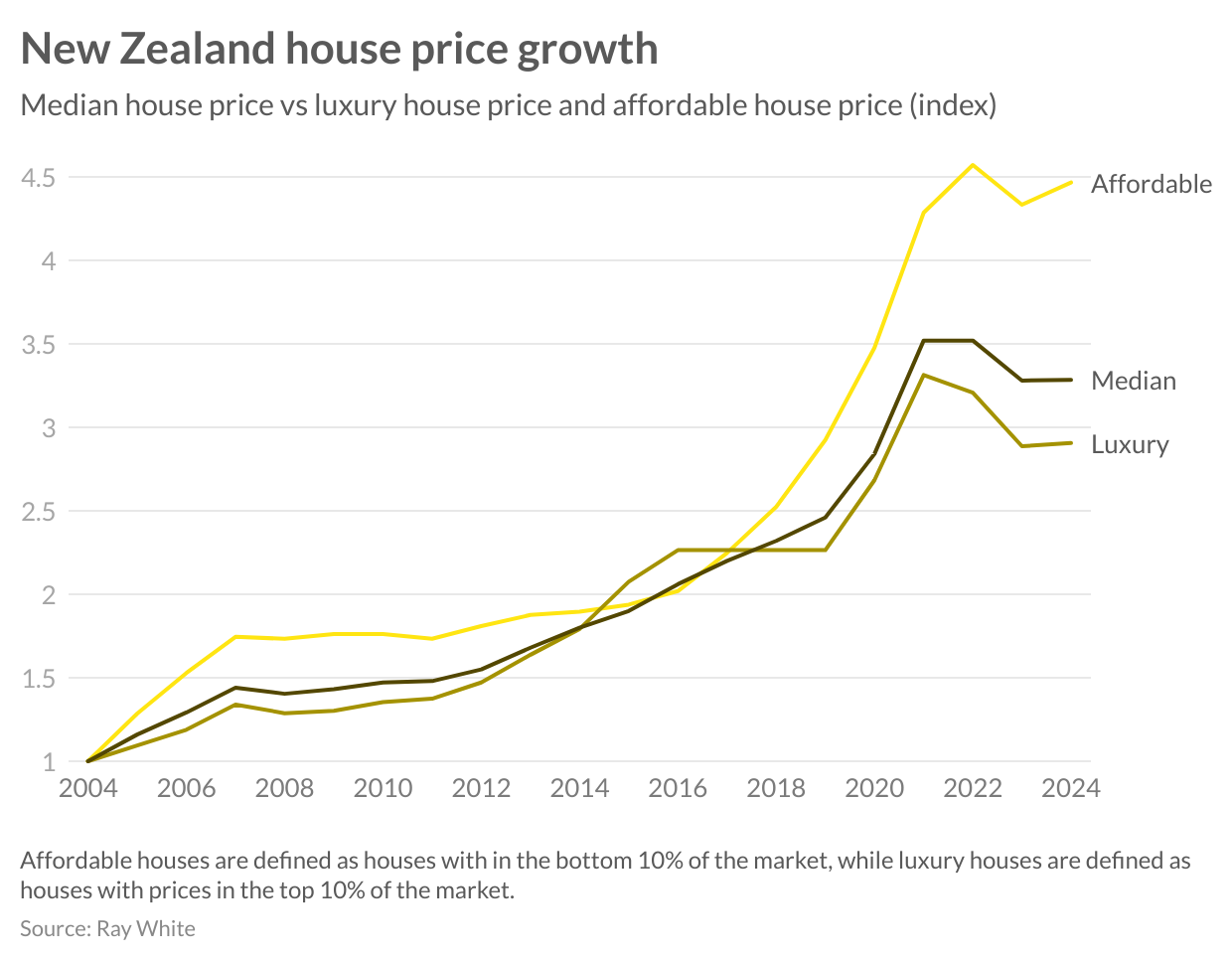

New Zealand’s housing market over the past two decades tells a compelling story of changing dynamics across different price segments. This analysis examines three distinct market segments: the affordable segment (representing houses priced in the bottom 10 per cent of the market), the median segment, and the luxury segment (comprising houses in the top 10 per cent of the market).

The first decade, from 2004 to 2014, was characterized by the affordable segment experiencing occasional spikes in prices, followed by periods of stabilization. This pattern reflected a market that, despite its fluctuations, remained relatively balanced across price points.

However, the second decade, from 2014 to 2024, marked a dramatic shift in the affordable segment, which demonstrated extraordinary growth without any significant periods of slowdown. Houses in this segment more than doubled in value, rising from $199,000 in 2014 to $469,000 in 2024. In contrast, both the median segment and luxury segment only saw strong growth in the first half of the decade but saw their momentum slow and reverse after 2020.

This shift is largely attributed to “mortgage fatigue,” where rising interest rates disproportionately impact owners of expensive homes due to their larger mortgages and higher monthly payments. As a result, demand for luxury properties has cooled, while more affordable homes have become increasingly attractive to buyers. The widening cost gap between a newly built home and existing homes has also influenced buyer behaviour. Established properties in the affordable segment are seeing heightened interest due to their relative affordability and location in developed neighbourhoods.

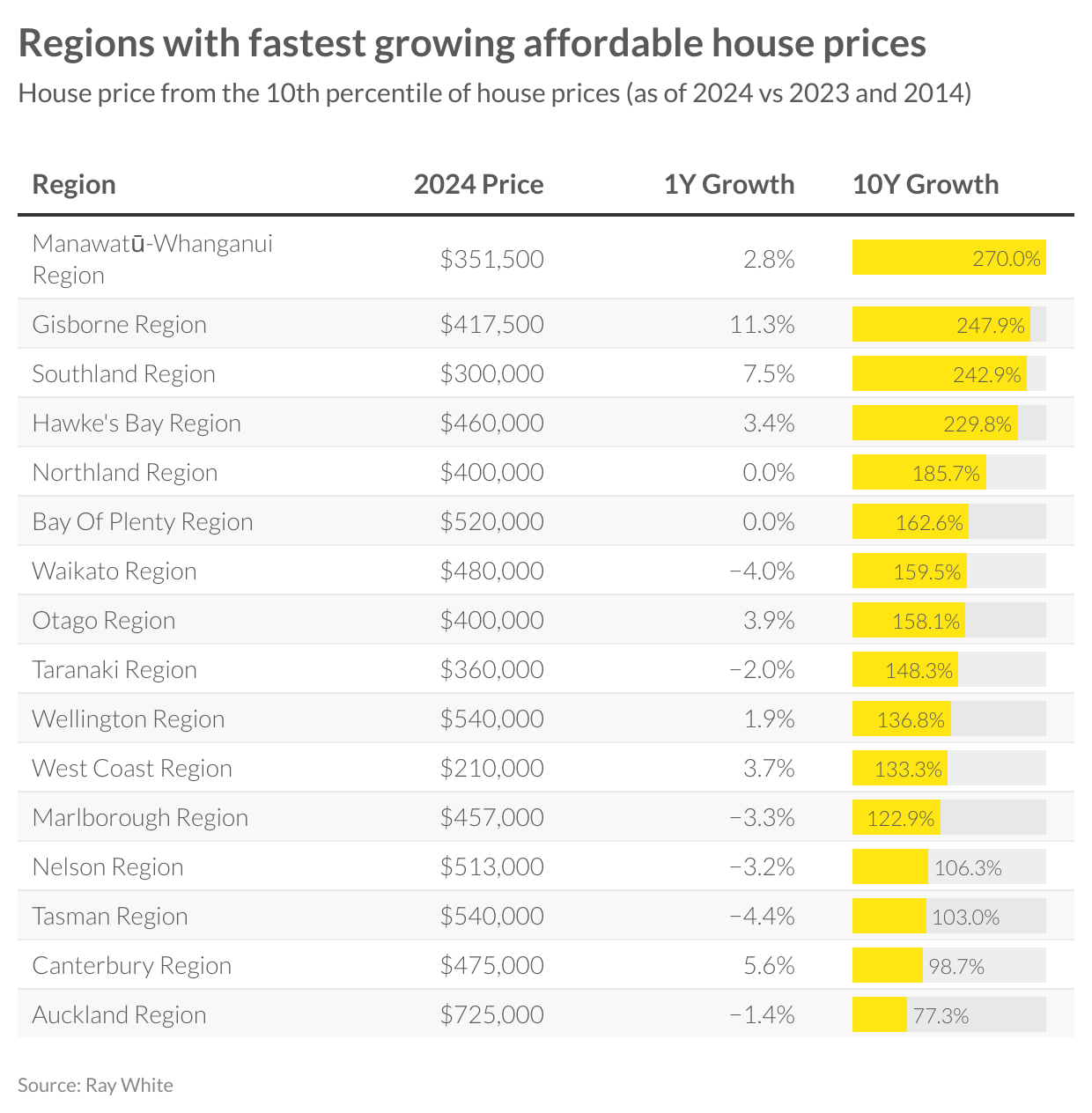

This national trend of affordable housing outperformance is more pronounced when examining regional markets. The Manawatū-Whanganui region emerges as the standout performer in the affordable housing segment, where entry-level homes have surged by an extraordinary 270 per cent.. In this region, the most affordable 10 per cent of houses, which were priced at just $95,000 a decade ago, now command $351,500. Following closely behind, regions like Gisborne, Southland, and Hawke’s Bay have seen their affordable housing segments transform dramatically, each recording growth exceeding 200 per cent.

Auckland, despite (or because of) having the highest entry-level prices, has shown the smallest decade-long growth at 77 per cent and has even declined by 1.36 per cent in the past year. At the other end of the spectrum, the West Coast maintains its position as the region with the most accessible entry point to homeownership, with its bottom 10 per cent of houses priced at $210,000. Although, even here, affordable homes have seen a 133 per cent increase over the decade.

These regional variations provide crucial context to the national trends. The implications are significant: the entry point to homeownership has risen dramatically across all regions, with the most affordable homes in some areas now priced at levels that would have been unthinkable a decade ago. This transformation represents a fundamental shift in New Zealand’s housing market dynamics, where the traditionally more affordable segments have shown the most dramatic appreciation.

Media contacts:

Atom Go Tian

Senior data analyst

Ray White Group

+61 422 089 938

agotian@raywhite.com

Cassandra Glover

Senior media advisor

Ray White Group

+61 447 000 472

cglover@raywhite.com